The Summer Opportunity: What Q3 Means for Town and City Centre Performance

As town and city centres enter the third quarter of the year, attention is firmly focused on the opportunities the summer period may present. Longer days, warmer weather and an expanding programme of leisure and social activity are expected to encourage consumers back into town and city centres for shopping, dining, entertainment, leisure and work.

While the UK economy showed encouraging resilience during Q1 2026, with GDP returning to growth, consumer confidence remains fragile and is currently at its lowest level since October 2023. Against this backdrop, understanding the significance of summer trading has become increasingly important for destinations seeking to maximise commercial performance during the second half of the year.

Analysis of Beauclair sales data from 2023–2025 provides valuable insight into the role the summer period plays within the annual trading cycle for town and city centres — and the scale of opportunity it may present in 2026.

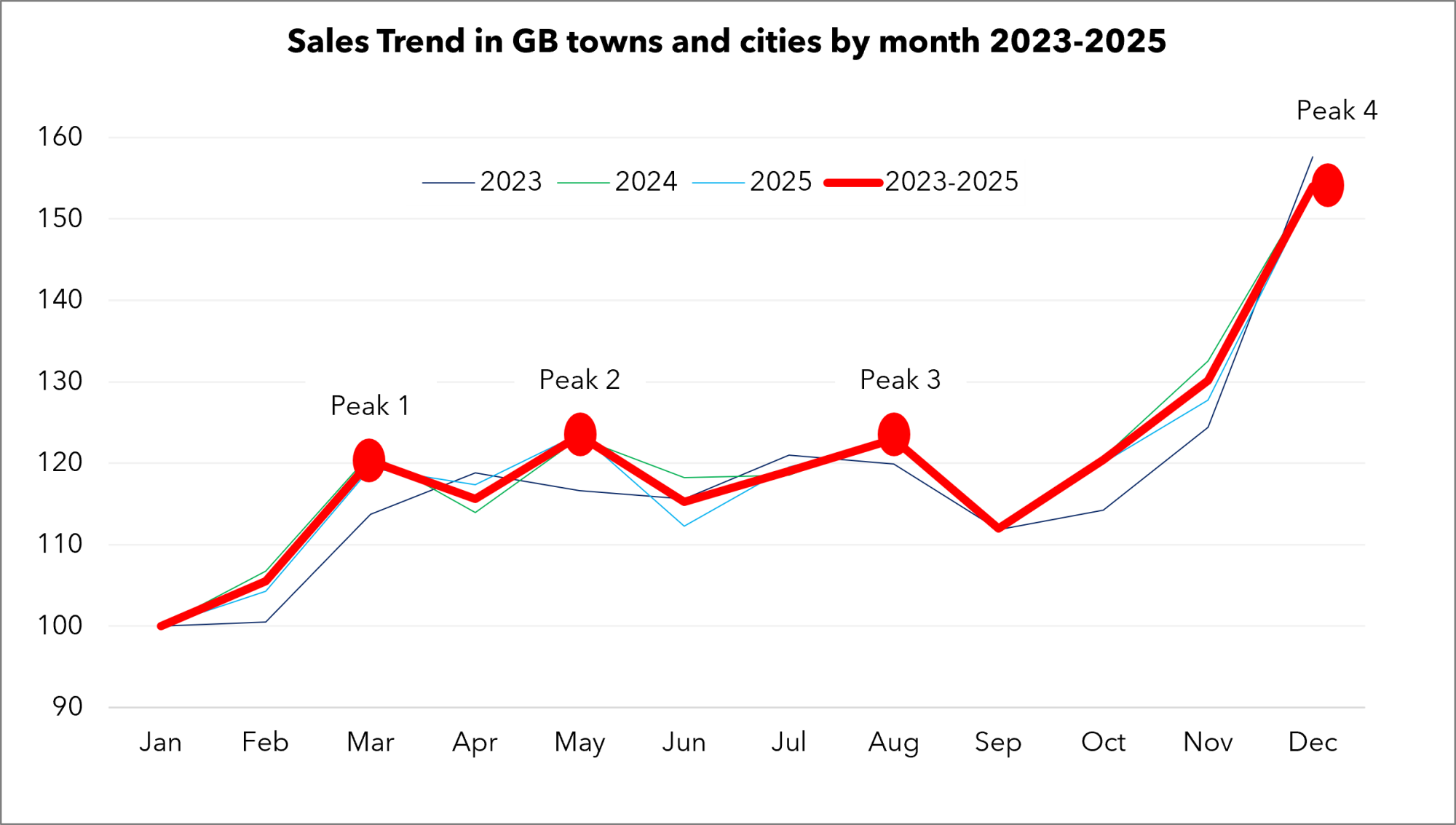

Four Key Trading Peaks

The data identifies four clear seasonal peaks in sales activity across the year: March/April (depending on the timing of Easter), May, August and December. While the first three peaks are relatively comparable in scale, December continues to dominate as the single most significant trading period of the year.

Over the past three years, sales increased by an average of 40% between October and December, compared with a more modest average uplift of 6.5% between June and August. Nevertheless, summer remains an important growth period for many locations, with historical trends showing sales typically building steadily through June and July before peaking in August.

Summer Growth Driven by Customers and Transactions

Importantly, summer growth is being driven primarily by increases in customer volumes and transaction activity rather than higher spend per visit. Average transaction values have remained broadly static during the summer months, rising by only 1.3% on average between July and August over the past three years.

For most towns and cities, this reinforces a clear commercial priority: attracting more customers, increasing dwell time and encouraging greater frequency of spend will be critical to maximising performance during Q3.

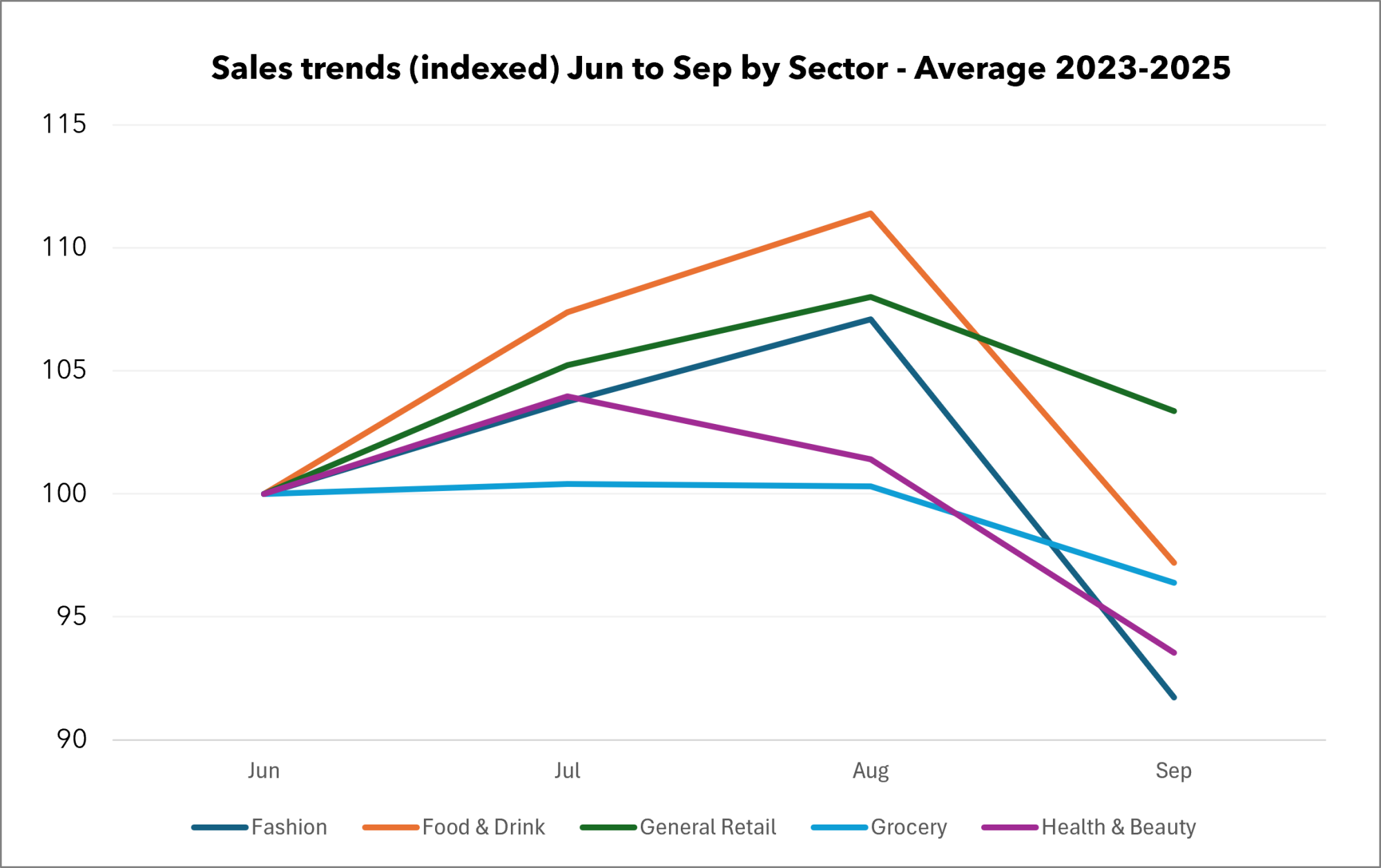

Which Sectors Perform Best During Summer?

Sector performance data highlights where the summer uplift is most likely to be concentrated.

Food & Drink — already the largest contributor to town centre expenditure, accounting for 25% of total sales compared with 20% for Fashion — consistently delivers the strongest summer growth performance.

Between 2023 and 2025, Food & Drink sales increased by an average of 11.7% between June and August, outperforming all other major sectors. General Retail followed with growth of 8.1%, while Fashion recorded growth of 7.2%.

Grocery sales remained broadly flat over the period, while Health & Beauty delivered only modest growth of 1.3%, driven primarily by pre-holiday spending between June and July before softening during August.

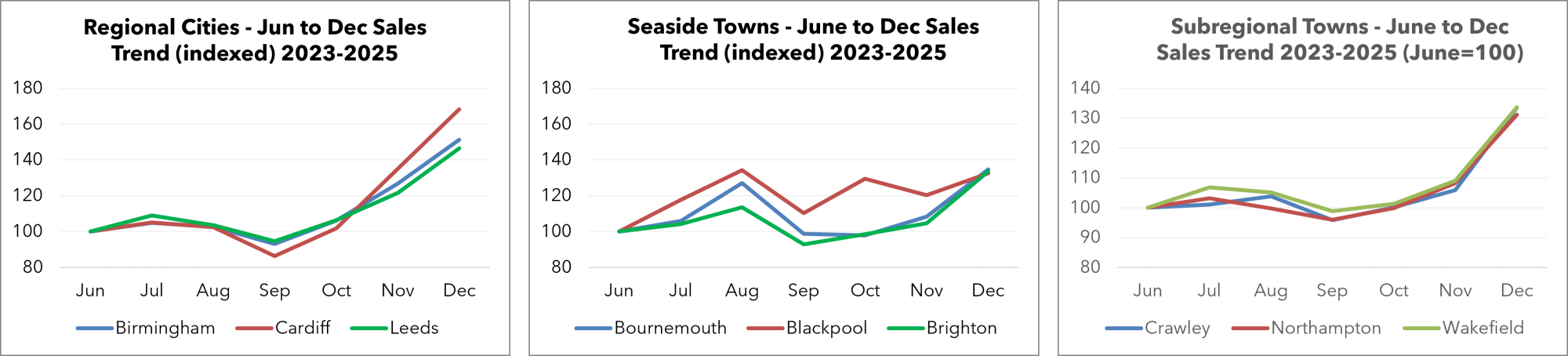

Summer Trading Patterns Differ by Location Type

National trends, however, only tell part of the story. The significance and timing of summer trading varies considerably depending on location type.

Analysis of sales trends between 2023 and 2025 across a sample of regional cities, seaside towns and subregional towns within the Beauclair GB Benchmark highlights clear differences in seasonal trading patterns.

In regional cities, sales typically peak in July before easing during August, likely reflecting the impact of residents and office workers taking holidays during the school summer break.

By contrast, seaside towns experience a much stronger late-summer uplift, with sales accelerating sharply during August as tourism, day trips and overnight stays increase.

Subregional towns generally follow a similar pattern to regional cities, with sales peaking in July in two of the three benchmark locations analysed. Crawley was the exception, where sales peaked in August, although this was largely influenced by an unusually strong August performance during 2024.

Summer Versus Christmas Trading

The relative importance of summer trading compared with Christmas also differs significantly across location types.

In several seaside destinations, summer trading now rivals — and in some cases exceeds — Christmas trading performance. Beauclair data shows that August sales exceeded December sales in both Bournemouth (+2%) and Blackpool (+9%), while Brighton recorded December sales only 14% above August levels.

In contrast, regional cities remain heavily reliant on Christmas trading, with December sales substantially outperforming August in Birmingham (+53%), Cardiff (+71%) and Leeds (+46%).

Subregional towns sit somewhere between these two extremes. In Crawley (+35%), Northampton (+28%) and Wakefield (+34%), the uplift between August and December is considerably less pronounced than in regional cities, but still greater than in seaside destinations.

What This Means for Town and City Practitioners

While there are four identifiable trading peaks nationally, the scale and significance of these peaks vary considerably by location type. For regional cities, Christmas continues to dominate annual trading performance. In seaside towns, however, August increasingly represents the single most important commercial opportunity of the year. Subregional towns sit somewhere between the two, with a less pronounced contrast between summer and Christmas trading peaks.

For town and city practitioners, the implications are significant. Understanding the specific dynamics of summer trading within a location is critical in shaping investment priorities, marketing activity and intervention strategies for the second half of the year. Key questions include how much emphasis and funding should be directed towards Q3 activity relative to the Christmas period, which sectors are likely to experience the greatest opportunities or pressures, and which businesses may require the most support — and when.

Beauclair’s data also highlights that summer growth is driven primarily by increased customer volumes rather than higher spend per transaction. As a result, attracting more spending visitors will remain central to driving commercial performance during Q3.

However, increasing spend per visit should not be overlooked. Encouraging higher transaction values provides an opportunity to grow sales without placing additional operational pressure on businesses already managing increased customer volumes.

A key part of this will be extending dwell time. Longer visits not only increase overall spend but also help distribute expenditure across a wider range of sectors and businesses. Locations that successfully combine strong customer numbers with compelling consumer experiences will be best placed to maximise sales performance, strengthen business resilience and deliver stronger returns on investment during the summer trading period.